Clerky vs. Startup Attorney: When Founders Should Hire a Lawyerfor Delaware C-Corp Formation

Clerky can generate Delaware C-Corp templates, but no attorney reviews your specific situation, and you cannot request custom legal changes or ask company-specificl egal questions.

A startup attorney adds custom IP assignment, equity structuring, QSBS and Section 351 analysis, vesting review, and 83(b)election tracking across each tranche.

The dollar gap can be small compared to the cost of a formation error. Boutique flat fees may run $1,500 to $3,500, while a single formation error can become expensive during Series A diligence or an acquisition.

Use an online incorporation platform if you are a solo technical founder with standard vesting, no pre-incorporation IP, and no near-term raise.

Hire startup counsel if you have co-founders, prior-employer IP, investors in conversation, QSBS planning needs, or operations in Arizona or California.

What This Comparison Actually Covers

Both Clerky and a startup attorney can help you file a DelawareC-Corp. You end up incorporated either way, with a Certificate of Incorporation accepted by the state and an entity that can sign contracts and raise money.The price difference answers only part of the question. What separates these paths is the legal risk that survives the filing.

Clerky generates documents from templates. When your situation matches the template, the output may be sufficient. When it does not, the gap can stay hidden until investor counsel reads your documents line by line during diligence. A pre-seed founder rarely sees the risk at formation because the documents may look complete. The cost often shows up later, when an unassigned piece of IP, missing vesting terms, an 83(b) issue, or an incomplete stock issuance becomes a diligence problem.

The decision is not simply whether to spend less at formation.The better question is: which legal issues are you willing to discover eighteen months from now, when investors or buyers are reviewing your company?

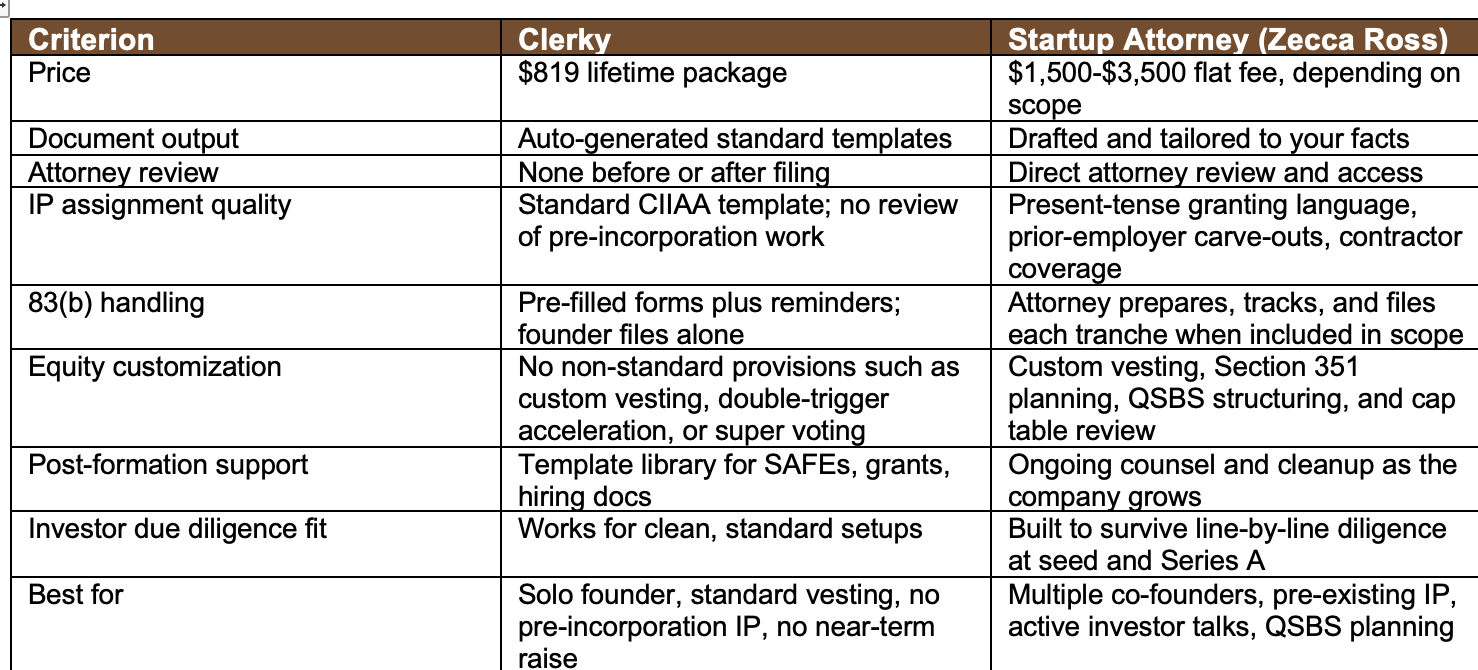

Snapshot: Clerky vs. a Startup Attorney

Both Clerky and a startup attorney can help create a filedDelaware C-Corp. The table below shows where they typically diverge.

How These Criteria Were Chosen

Every criterion below answers one question that a venture investor, buyer, or diligence counsel may ask during seed, Series A, or acquisition diligence. Investors and buyers review formation documents, capitalization records, IP ownership, stock issuances, vesting, contracts, and board approvals. The gaps they find can determine whether a deal closes, stalls, is repriced, or requires cleanup before closing.

The features compared here track issues that commonly surface in diligence: IP assignment quality, 83(b) execution, vesting enforceability, equity issuance records, state compliance, and investor-ready corporate records. A feature that never appears in diligence is less important than a document or approval that investor counsel will request.

What Clerky Actually Produces

Clerky’s formation package can generate the document stack a Delaware C-Corp needs to exist on paper. That may include a Certificate of Incorporation, bylaws, written consent of the incorporator, board consent, founder stock purchase agreements with vesting, a CIIAA that assigns intellectual property to the company, and pre-filled 83(b) election forms withreminders.

Post-formation, the platform may also support SAFEs, convertible notes, equity grants, advisor agreements, and maintenance filings. The templates may be well-drafted for standard facts, and for a founder whose situation matches the template, that output may be filing-ready.

The boundary sits at the word standard. No attorney reviews your specific documents before or after filing because Clerky is not your law firm. You cannot ask a platform to evaluate an unusual fact, draft around a prior-employer IP issue, revise a clause for a custom vesting arrangement, or advise whether a multi-founder equity split needs a provision the template does not contemplate.

That gap matters because templates can only process the information a founder enters. They cannot determine whether the facts entered are the right facts for the company, whether pre-incorporation code ha sactually been assigned, or whether the founder’s fundraising, QSBS, or statecompliance plans require a different structure.

What a Startup Attorney Provides That Clerky Cannot

An attorney can draft assignment language in the present tense so the founder or contractor “hereby assigns” IP to the company rather than merely promising to assign it later. That distinction matters in diligence because ambiguous assignment language may trigger a request for confirmatory assignment before closing.

IP Assignment: Where Template Documents Break Down

For technology, AI, SaaS, biotech, and product startups, intellectual property is often the company’s most important asset. The company may need to prove that it owns the software, data, designs, inventions, trade secrets, technical documentation, brand assets, customer lists, and other materials that make the business valuable.

The issue is simple: forming a corporation does not automatically transfer IP to the corporation. If a founder built code before incorporation, if a contractor wrote software, if a university lab or prior employer had rights, or if a consultant contributed core technology, the company may not fully own what it needs to operate unless the right written assignments are signed.

Employees may create work that belongs to the employer within the scope of employment, but independent contractors are different. Contractor-created software may remain with the contractor unless a written agreement assigns it to the company. A standard CIIAA may cover a signing founder going forward, but it may not capture a contractor who never signed, a consultant who left, or technology created before the company existed.

The fix for missing IP assignment is often harder later. Present-tense granting language can transfer rights when signed. Language that only promises to assign later, or language that is ambiguous, may require a confirmatory assignment. If the contributor has left, moved, or knows the company is raising capital or selling, that signature may become expensive or unavailable.

83(b) Elections: The 30-Day Cliff No Platform Can Enforce

For founders receiving restricted stock, that deadline matters. If the stock vests over time and no timely 83(b) election is filed, each vesting tranche may create taxable income based on the value at the time of vesting rather than the low value at issuance. If the company increases invalue, the tax burden can become significant.

Online platforms may pre-fill the 83(b) form and send reminders, but the founder usually remains responsible for printing, signing, mailing or filing, and confirming the election within the deadline. A reminder is not a filing.

A boutique startup attorney can prepare the packet, track the 30-day window, and help manage filings for each tranche when included in the scope. When founder stock is issued in more than one tranche, each issuance may require separate attention. This is administrative work with little margin for error.

Equity Structure and Vesting: Standard Templates vs. Your Actual Cap Table

Standard founder stock purchase agreements often use a four-year vesting schedule with a one-year cliff. That is familiar to investors and may work for a clean single-founder or simple co-founder setup. The problem is not the default structure itself. The problem is knowing whether the default belongs in your documents at all.

A template cannot make the judgment calls that protect the company when facts are not standard. For example, founders may need custom vesting, repurchase rights, treatment for a departing founder, double-trigger acceleration, super voting shares, or a multi-class capital structure. Each of those choices depends on the company’s facts, fundraising plan, and long-term control considerations.

Because qualification depends on issuance, entity type, ownership, business activity, and asset thresholds, founders should not assume their stock qualifies. A startup attorney and tax advisor can help structure and document the issuance so the company has a stronger record if QSBS is later reviewed.

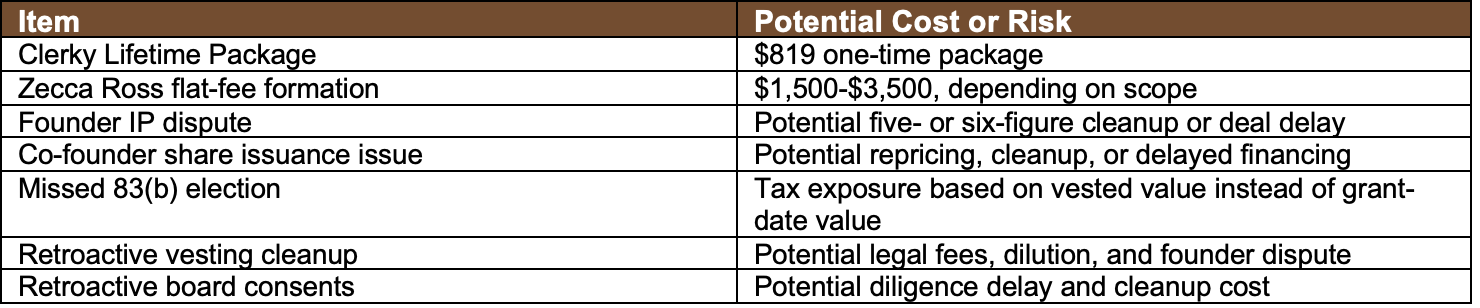

Cost Comparison: Upfront Fees vs. Total Formation Risk

Clerky’s filing cost may look attractive next to a $1,500 to$3,500 attorney flat fee. That comparison is useful only if the company remains simple and never faces serious diligence. The moment investor counsel examines the cap table, IP records, and approvals, the relevant number becomes the cost to fix what the template missed.

The downstream costs are not always predictable, but the categories are familiar. Missing IP assignments, unclear founder equity, missed 83(b) filings, retroactive board approvals, and inaccurate cap tables can allbecome expensive when the company is raising capital or selling.

The honest comparison is not only $819 against $3,500. It is the cost of certainty now against the risk of cleanup later, when valuation is higher, investor counsel is waiting, and the deal clock is running.

When Clerky Is the Right Call

Clerky may be the right tool for a solo technical founder who wrote all the code after incorporation, accepts a standard four-year vesting schedule with a one-year cliff, has no contractors or outside contributors, has no prior-employer IP issue, and has no near-term plans to raise outside capital.

If you own everything you contribute, hold all the equity yourself, and need no non-standard provisions, the template stack may produce what you need to get started. The risk increases when your facts stop matchingthe template.

When to Hire a Delaware Incorporation Lawyer

Hire a Delaware incorporation lawyer when your formationinvolves any fact a template cannot read. Multiple co-founders splittingequity, code or research built before incorporation, a prior employer’s IPagreement, live investor conversations, QSBS planning, or Arizona andCalifornia operations all create questions that require legal judgment.

These issues become the exact diligence questions investors andbuyers ask first. Missing IP assignment, unclear founder equity, incompletestock issuance records, or state registration gaps can delay a financing oracquisition even when the business itself is strong.

Best fit for attorney-led formation: founders with co-founders, pre-existing or prior-employer IP, active fundraising conversations, QSBS planning needs, or Arizona and California operations requiring foreignqualification.

Zecca Ross Flat-Fee Incorporation Packages

Zecca Ross Law Firm handles Delaware C-Corp formation and startup legal matters on a flat-fee or defined-scope basis when appropriate. Pricing depends on the number of founders, the equity structure, the IP history, state compliance needs, and whether pre-incorporation cleanup is required.

A founder-focused formation scope may include the Certificate of Incorporation, bylaws, organizational consents, founder stock purchase agreements with vesting, IP assignment documentation, EIN coordination, registered agent coordination, Delaware franchise tax setup, 83(b) election support, and review of state compliance considerations.

The firm works with founders in Arizona, California, and across the United States, including international founders forming U.S. companies. A founder operating in Arizona or California can benefit from Delaware corporate structure and home-state compliance guidance from the same legal team.

Related Startup Legal Services

If you are forming, reviewing, or preparing your startup for growth, Zecca Ross Law Firm can assist with:

Startup and business legal services for formation, contracts, cap tables, governance, fundraising readiness, and M&A.

Post-formation legal review for founders who already incorporated and want attorney review of documents and compliance.

Startup contracts and IP protection for IP assignments, contractor agreements, SaaS contracts, confidentiality agreements, terms of use, and privacy policies.

Cap table cleanup and founder equity review for stock issuances, SAFEs, advisor equity, option plans, and diligence readiness.

M&A and acquisition readiness for startupspreparing for asset sales, stock sales, diligence, disclosure schedules, andclosing support.

Schedule a consultation to discuss your formation, equity, contracts, cap table, financing, or M&A needs.

FAQs

Can I use Clerky and then hire a lawyer to review it?

Yes. Many founders form a company first and later hire a startup attorney to review the documents. An attorney can review formationdocuments, founder stock records, IP assignments, 83(b) records, cap tables,and compliance items before they surface in investor or buyer diligence. ZeccaRoss Law Firm can assist with startup legal review and cleanup.

Does Clerky’s CIIAA cover pre-incorporation IP?

Not always. A standard Confidential Information and Invention Assignment Agreement may cover work created after signing, but pre-incorporation IP, contractor-created work, university-related work, or prior-employer issues may require specific assignment language. A startup attorney can draft assignment language to capture the IP the company actually needs.

What happens if I miss the 83(b) deadline?

The IRS filing deadline is generally 30 days after the restricted stock or other property is transferred, as described in IRS Form 15620. If the deadline is missed, the founder may lose the ability to elect tax treatment based on the grant-date value and may face tax consequences as the stock vests.

Do I need a Delaware lawyer if I am in Arizona or California?

You need counsel who understands both Delaware corporate structure and the state where the company actually operates. Delaware incorporation governs the corporate charter, but Arizona, California, or another operating state may require foreign qualification, tax registration, employment compliance, or other state-level steps.

How does QSBS affect my formation decision?

QSBS planning under Internal Revenue Code Section 1202 can be valuable, but qualification depends on the company, the stock, the issuance, the shareholder, and the business activity. Founders should coordinate with startup counsel and tax advisors before assuming their stock qualifies.

When should I contact a startup attorney?

Contact a startup attorney before issuing founder stock,assigning IP, hiring contractors, raising capital, signing investor documents,or preparing for acquisition diligence. You can contactZecca Ross Law Firm to discuss your startup’s formation and legalreadiness.

Legal Disclaimer

This article is for general informational purposes only anddoes not constitute legal, tax, or investment advice. Reading this article doesnot create an attorney-client relationship. Founders should consult qualifiedlegal and tax advisors regarding their specific facts.

Suggested External References

IRS Form 15620 - Section 83(b) Election

17 U.S.C. Section 101 - Copyright definitions and workmade for hire concepts

26 U.S.C. Section 351 - Transfer to corporationcontrolled by transferor

26 U.S.C. Section 1202 - Qualified Small Business Stock

Legal clarity starts here. Partner with Zecca Ross Law Firm to transform complexity into opportunity.